Introduction:

Securing a mortgage can be a challenging process, especially for individuals with limited credit history, low credit scores, or insufficient income. To help bridge the gap and increase approval chances, co-signers and guarantors play essential roles in the mortgage industry. In this blog post, we’ll explore everything you need to know about these two roles, their advantages, disadvantages, and key tips for those contemplating co-signing or guaranteeing a mortgage.

- a co-signer, also known as a co-borrower, is an individual who joins the primary borrower (typically the homebuyer) in applying for a mortgage. The co-signer has an equal ownership interest in the property financed by the mortgage and shares equal responsibility for repaying the loan. Essentially, the co-signer’s role is to provide additional financial support and credibility to help the primary borrower qualify for the mortgage. This arrangement can be particularly beneficial when the primary borrower’s credit history, income, or financial situation may not meet the lender’s requirements on their own. Co-signing effectively combines the creditworthiness and financial resources of both the primary borrower and the co-signer to strengthen the mortgage application and improve the chances of approval. However, it’s important to note that co-signers are equally liable for the mortgage debt, which means they are legally responsible for making payments if the primary borrower defaults.

when someone co-signs on a loan or credit account, it can appear on their credit reports. Co-signing essentially means that the person is equally responsible for the debt, and therefore, it is considered a part of their credit history. This information is typically found on their credit report and can impact their credit score.

The co-signer’s credit report will show the same account information as the primary borrower’s credit report, including the account type, payment history, and outstanding balance. Co-signers need to be aware that any missed or late payments on the co-signed account will also be reflected on their credit report, potentially affecting their credit score.

- a guarantor is an entity or individual who offers a financial guarantee to a lender on behalf of the primary borrower, typically a homebuyer. This guarantee assures the lender that the mortgage will be repaid even if the primary borrower defaults. Unlike co-signers, guarantors do not have joint ownership or shared responsibility for the mortgage, but they pledge to cover the debt in case of payment delinquency by the primary borrower. Guarantors are often used when the primary borrower’s creditworthiness or financial situation falls short of the lender’s requirements, providing additional assurance and increasing the likelihood of mortgage approval.

Guarantors in the context of mortgages or loans are financially responsible for repaying the debt if the primary borrower defaults. Their liability entails covering the outstanding balance and making mortgage payments as agreed with the lender. Guarantors are legally bound to fulfill this obligation, ensuring the lender is repaid, and they may face legal consequences if they fail to do so.

Co-signers and guarantors both play a role in helping someone secure a loan or credit, but there are some key differences between the two:

- Primary Responsibility:

- A co-signer is equally responsible for the debt and has a share of the ownership in the account. If the primary borrower defaults, the co-signer is expected to make payments.

- A guarantor is not a joint owner of the account. Instead, they provide a guarantee that they will cover the debt if the primary borrower defaults.

- Ownership and Liability:

- A co-signer has a legal interest in the property or asset financed by the loan. For example, if they co-sign a car loan, they have an ownership interest in the car.

- A guarantor does not have ownership interest in the asset but is responsible for repaying the debt if the primary borrower fails to do so.

- Credit Reporting:

- Both co-signers and guarantors can have the loan or credit account appear on their credit reports, including the payment history and outstanding balance.

- The impact on the credit reports of co-signers and guarantors is similar. Any late or missed payments on the guaranteed account can negatively affect their credit scores.

- Responsibility Level:

- Co-signers are typically brought in when the primary borrower’s creditworthiness or income is insufficient to secure the loan. They are seen as equally responsible for the debt.

- Guarantors may be used in cases where the primary borrower doesn’t have a sufficient credit history, but the guarantor’s role is generally more about providing a financial guarantee rather than sharing equal responsibility for the debt.Co-Signers:

Advantages:

- Enhanced Borrowing Capability: Co-signers can help borrowers with limited credit history or lower credit scores qualify for loans they might not otherwise be eligible for.

- Better Loan Terms: With a co-signer, borrowers may secure loans with more favorable terms, such as lower interest rates.

- Credit Building: Timely payments on the co-signed account can positively impact the co-signer’s credit score.

Disadvantages:

- Shared Responsibility: Co-signers share equal responsibility for the debt. If the primary borrower defaults, the co-signer is on the hook for the payments.

- Credit Risk: Any late payments or defaults on the co-signed account will negatively affect the co-signer’s credit score.

- Legal Obligations: Co-signers can be pursued for payment by creditors and may face legal consequences if the debt is not repaid.

Guarantors:

Advantages:

- Indirect Responsibility: Guarantors are not joint owners of the account, making their role less financially involved.

- Assisting Credit Applicants: Guarantors can help individuals with limited or poor credit history qualify for loans without taking on shared ownership of the debt.

Disadvantages:

- Liability: While less directly involved, guarantors are still legally obligated to cover the debt if the primary borrower defaults.

- Credit Impact: Late payments or defaults by the primary borrower can negatively affect the guarantor’s credit score.

- Limited Control: Guarantors typically have less control over the account and may not be informed of the primary borrower’s payment status.

Tips for Co-Signing or Guaranteeing:

- Know the Borrower: Understand the financial responsibility and reliability of the person you’re assisting.

- Open Communication: Maintain clear communication with the primary borrower to monitor their repayment.

- Set Limits: Consider setting limits on the amount you’re willing to co-sign or guarantee.

- Exit Strategy: Discuss an exit plan with the primary borrower, such as refinancing the loan in their name.

- Legal Advice: Consult with a legal or financial professional to understand your rights and responsibilities fully.

Conclusion: Co-signing and guaranteeing loans can be a great way to help a friend or family member obtain financing when they might not otherwise qualify. However, both roles come with financial and credit-related responsibilities. It’s crucial to weigh the advantages and disadvantages carefully and consider the potential impact on your credit. Clear communication and a solid understanding of your obligations are key to ensuring a successful co-signing or guaranteeing arrangement. Remember, your financial health matters too, so proceed with caution and thoughtfulness.

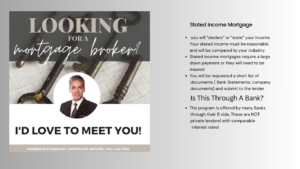

The Stated Income Program is tailored to meet the unique needs of individuals whose income might not fit the mold of traditional employment. Here are some of the key groups that can benefit:

The Stated Income Program is tailored to meet the unique needs of individuals whose income might not fit the mold of traditional employment. Here are some of the key groups that can benefit: In the Stated Income Program:

In the Stated Income Program: